Real estate syndicators face financial reporting, liquidity, and investor-relations risk when capital call accounting is handled poorly. Precisely tracking these capital movements is critical for maintaining investor trust, and is a core component of professional real estate syndication accounting services.

Strengthen your capital call controls with DMR Consulting Group real estate CFO services.

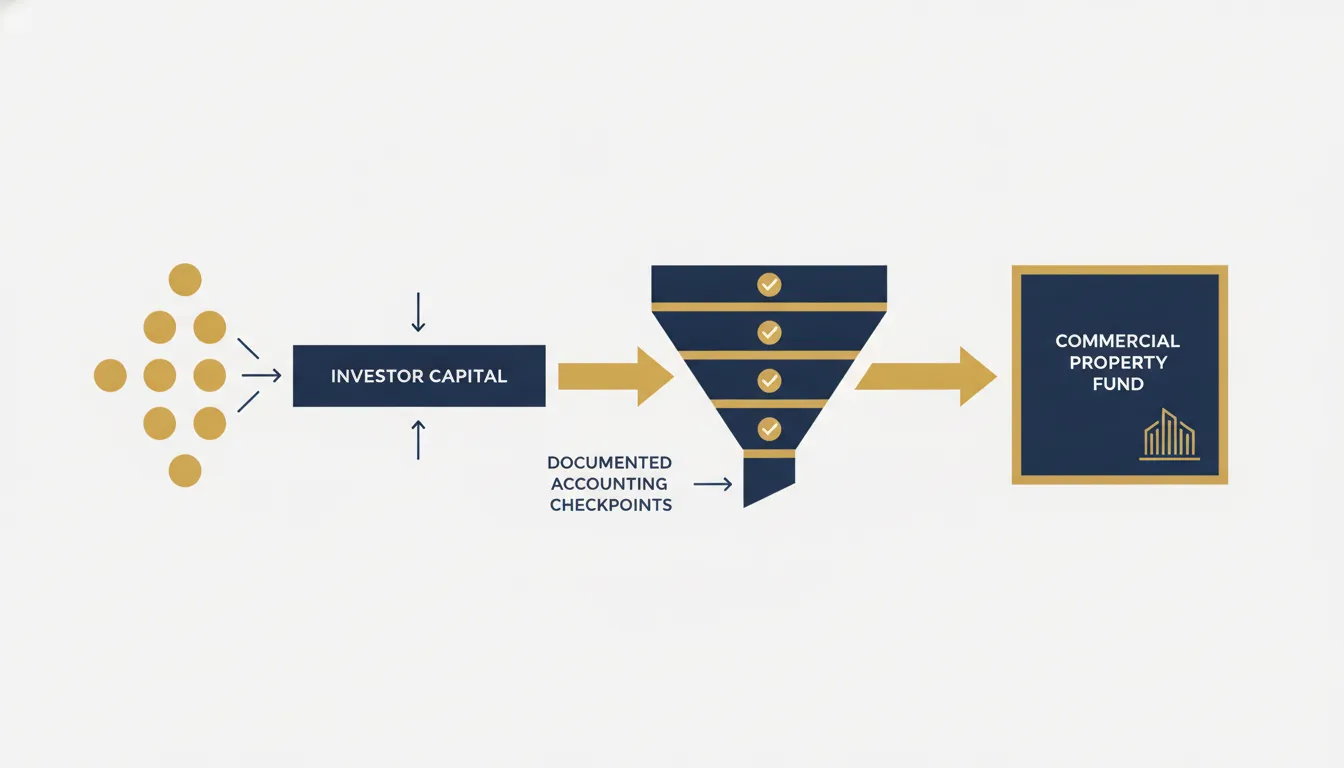

Capital call accounting is the process of tracking and recording the money real estate syndicators request from their investors to fund specific project needs. This accounting method ensures that every dollar moving from a commitment to an active investment is properly documented in the fund’s ledger. According to the SEC, private funds typically accept capital commitments and call down funds from investors over time as they find new deals to buy. For real estate syndicators, this means managing the timing of notices, recording cash receipts, and updating each investor’s capital account balance. Precise records help operators manage cash flow, calculate preferred returns, and maintain transparent reporting for their limited partners. By keeping clean books, syndicators can avoid the control failures and reporting errors that often plague growing real estate investment funds.

Growing your fund depends on how well you handle these complex financial entries. You must understand how these drawdowns work to keep your investors confident and your records clean. The next step is to understand What is capital call accounting in a real estate syndication? and how it impacts your fund. The answer begins with

What is capital call accounting in a real estate syndication?

Capital call accounting is the control framework used to track investor commitments, approved drawdowns, cash receipts, and remaining uncalled capital. An investor may commit a defined amount at closing, while the sponsor draws capital only as acquisition, improvement, reserve, or operating requirements arise. The accounting process connects each commitment to the related notice, receipt, ledger entry, and investor capital account.

Distinguishing commitments from funded capital

A fund begins with documented investor commitments. The U.S. Securities and Exchange Commission explains that private funds commonly accept commitments and draw capital over time. Until a drawdown occurs, the commitment generally belongs in a memorandum or investor-subledger record rather than available cash. That distinction helps management assess liquidity for acquisitions, capital improvements, reserves, and operating requirements.

When approved funding is required, the sponsor issues a capital call notice, also called a drawdown notice. The accounting team then tracks the receivable or expected contribution, cash receipt, and investor capital-account update under the fund’s documented accounting policy. Clear capital call accounting steps show each investor how much has been funded and what remains uncalled.

Capital call lifecycle and control points

The capital call cycle begins with an approved notice that states the amount, purpose, allocation by investor, payment instructions, and due date. The accounting treatment and recognition date should follow the fund’s documented policy and applicable reporting framework. Upon receipt, the team reconciles the wire, records the contribution, and updates the investor’s funded and unfunded balances.

Managing this cycle consistently supports reliable fund administration throughout a multi-year investment horizon. DMR Consulting Group’s accounting and CPA services help real estate operators establish disciplined close procedures, reconcile investor activity, and maintain decision-ready financial records. Accurate commitment and liquidity reporting also helps management prepare for the next acquisition without overstating available capital.

Posting contributions to the general ledger

When cash arrives, the accounting team should match the receipt to the applicable investor and drawdown before posting it under the fund’s chart of accounts and accounting policy. The related investor subledger must also reflect funded capital and the remaining commitment. This coordinated posting process keeps the general ledger, bank reconciliation, and investor records aligned.

Clean capital records also strengthen financing readiness. Lenders and other stakeholders may evaluate the fund’s liquidity, equity activity, controls, and reporting consistency during underwriting or diligence. Reconciled capital call records make those reviews more efficient and provide management a defensible view of available and uncalled capital.

Which records should you track during a capital call?

Track each investor’s total commitment, every drawdown amount and purpose, notice and due dates, receipt date, funding status, remaining uncalled capital, and related general-ledger entries. Reconcile those records to bank activity and the investor subledger so management can substantiate cash, equity, and investor reporting.

A defensible capital call control schedule captures the complete transaction trail from approved notice through receipt, reconciliation, and reporting. Maintaining that trail supports accurate capital accounts, reliable close procedures, and transparent investor communication. Following disciplined capital call accounting procedures ensures your fund stays on the right track.

Investor commitments, allocations, and notice details

The first record to track is the total capital commitment for each investor. You should maintain a subledger that shows the total amount an investor agreed to provide. When you issue a call, log the specific call amount, the due date, and the purpose of the funds. According to the SEC, private funds draw committed capital from limited partners as needed for investments or expenses. Having these fields in your tracker allows you to see how much uncalled capital remains in your fund at any time.

The schedule should also record the receipt date for each contribution. This information supports capital-account maintenance and the fund’s documented allocation methodology. If an investor is late, your records should show the delay. This tracking is key because the accounting entry for the contribution is usually effective on the due date stated in your capital call notice. Accurate logs help you manage cash flow across the full life of the fund, which can last 10 to 15 years.

Entity-level reconciliation and funding status

Once funds arrive, you must reconcile them at the entity level. This means matching the cash in your bank account to the investor subledger. You should track the funding status of each call, such as pending, received, or late. This clear view helps management identify exceptions promptly. Using these logs, you can build investor reports that lenders and partners will value. Precise records prevent errors in equity split calculations and ensure fair treatment for all partners.

Core fields for a capital call control schedule

To help you stay organized, use a standard set of fields for every call. The table below shows the core data points an operator should maintain for every investor transaction.

| Data Field | Record Type | Purpose |

|---|---|---|

| Commitment Total | Master Record | Tracks the full amount an investor agreed to provide. |

| Call Amount | Transaction | Shows the specific cash requested in a single call. |

| Due Date | Notice Detail | Sets the stated funding deadline for the fund transfer. |

| Receipt Date | Bank Record | Logs when the cash actually hit the fund account. |

| Funding Status | Operational | Flags if the payment is pending, paid, or late. |

| Remaining Balance | Subledger | Shows the uncalled capital left for the investor. |

By tracking these fields, you make the audit process much easier. You also ensure that your accounting and CPA services team has what they need to file tax returns on time. Reconciled records are the foundation of disciplined real estate syndication reporting.

How does the capital call accounting workflow work?

A controlled capital call workflow moves from liquidity forecasting and approval to notice issuance, cash receipt, bank reconciliation, ledger posting, investor-subledger updates, and management review. Each stage should have a responsible owner, supporting documentation, and a defined cutoff so the operator can produce consistent, auditable reporting.

Managing fund flows requires a controlled process. The capital call accounting workflow connects investor commitments to contributions for property acquisitions or approved fund costs. It tracks each drawdown from the initial notice through final reporting.

End-to-end drawdown workflow

Capital calls let fund managers draw capital from partners when it is time to buy a disciplined operatorperty or fund approved costs. Per the SEC, private funds often call down capital as needed over the life of the fund. This avoids having too much idle cash on hand before the team can put it to work.

- Notice sending: The fund manager sends a formal notice to all partners. This notice lists the total amount needed, the partner share, and the due date.

- Capital receipt: Partners send funds by wire or bank transfer. The team checks the bank account to confirm when each payment arrives.

- Entry writing: Once cash is received, the team posts the contribution to the general ledger. This often happens on the due date listed in the notice.

- Bank matching: The team matches the incoming wires to the bank statement. This step ensures the books match the actual cash held by the fund.

- Subledger updates: Each partner has their own subledger. The team records the payment to update the partner’s total stake and remaining pledge.

- Internal checks: Managers review the new cash level. They use this data to confirm the fund has sufficient liquidity for the planned acquisition.

Documented accounting policy and ledger entries

The exact capital call accounting procedures depend on the fund’s documented policies. Most fund managers treat capital commitments as memorandum records rather than recognized cash until a drawdown occurs. These commitments often remain in memorandum records or investor subledgers that track future funding capacity.

When the call is active, the team records a debit to the asset account and a credit to the bank or pledge account. The exact timing and account names must follow the fund’s documented policies. Consistent application supports clear records and a more efficient year-end audit.

Investor subledgers and reporting

Precise tracking for each partner is a core part of capital call accounting. Each investor needs visibility into funded capital and the remaining commitment. This data supports accurate allocations of future income, gains, and losses.

The workflow ends with clear reports to the partners. Investors expect confirmation that contributions were received and applied to the stated purpose. Consistent tracking supports confidence between the fund manager and investors throughout the life of the investment.

Why do timing and documentation matter?

Timing determines the reporting period, available liquidity, and investor funding status reflected in the books. Complete documentation connects the approved drawdown to its notice, receipt, ledger entry, and use of funds. Together, disciplined cutoffs and an audit trail reduce reconciliation breaks and improve investor-reporting reliability.

Precise timing and clear records are the backbone of any fund. When you manage a real estate group, your capital call accounting procedures must match the dates set in your governing documents. A missed cutoff or incomplete record can misstate investor reports. It can also weaken confidence and obscure the fund’s actual liquidity position.

Establishing a consistent reporting cutoff

A set cutoff date keeps your books clean. You should pick a firm time each month to close your files and stop taking new data. This helps you track capital commitments from your investors without mixing up old and new funds. Without a consistent cutoff, reports may not present an accurate view of the fund’s financial position. Clear timing ensures that every dollar is tied to the right asset at the right time.

Maintaining a complete audit trail

Maintain an audit trail for each fund transaction. Retain every capital call notice, bank confirmation, approval, and supporting cost schedule in a controlled repository. Complete records support properly accounting for capital calls during tax preparation, audit, lender diligence, or other financial review. If you use version control for your files, you can see how numbers changed over time. This audit trail protects the firm and provides investors reporting confidence.

Reconciling late or unmatched receipts

Late receipts can throw off your whole plan. You must match your bank records to your books every week to find gaps early. This task helps you catch late funds or missing costs before they grow into material issues. By staying on top of your files, you ensure your reports are always ready for the people who need them most.

Common capital call accounting mistakes to avoid

Managing capital calls for a real estate fund is a complex task. Small errors in capital call accounting can lead to material issues with your investors. To maintain reliable books and investor confidence, avoid these common control failures. Working with an expert can help you set up capital call accounting procedures that work.

Commitment tracking and liquidity forecasting

One common error is writing capital pledges as cash on hand. While an investor might pledge a large sum, that money is not in your bank account yet. As per the SEC, private funds accept these pledges and call them down only as needed. If you treat commitments as cash, the books can overstate liquidity. This mistake can lead to poor choices about property acquisitions or repairs.

Another issue is not planning for cash needs. You must know exactly when you will need funds for a deal. If you call for capital too late, you might miss a closing date. If you call it too early, you have cash sitting idle. Stale plans often cause these timing gaps. You should update your cash flow plans every month to stay on track.

Investor-level subledger integrity

Commingled or inconsistent investor logs can quickly undermine confidence. Each investor needs a clear trail of drawdowns and contributions. You must track every dollar from the first notice to the final receipt. If your logs do not match what your investors see, you will face detailed questions. Poor records also make it difficult to manage capital call accounting for syndications when you have many partners.

Unclear equity grouping is also a risk. You need to know which funds are debt and which are equity. Misclassification can distort tax reporting and investor statements. In many cases, these errors happen because the manager lacks a clear way to label funds. A standardized chart of accounts helps prevent inconsistent classification.

Cross-report reconciliation

Unmatched receipts are a common control exception for fund managers. When an investor sends money, you must tag it to the right call promptly. If you wait for three months, you might lose track of transaction details. You should match your bank records with your investor logs every week. This habit ensures that every payment is right before you move to the next phase.

Finally, avoid reporting totals that do not tie out. Your balance sheet, income statement, and investor reports must reconcile to a consistent financial position. If the total capital shown in your reports does not match your cash accounts, your data is flawed. These gaps often come from typing errors. Software or expert review can help you spot these errors early. Making sure you are properly accounting for capital calls ensures your reports are ready for any audit.

How CFO-level reporting supports investor confidence

CFO-level reporting connects capital administration to investor confidence and sponsor decision-making. The Securities and Exchange Commission explains that private funds often draw committed capital as investment opportunities arise. DMR Consulting Group helps operators convert bank activity, investor subledgers, forecasts, and property-level results into a coherent view of liquidity and fund performance.

Monitoring commitments, drawdowns, and liquidity

Good reports start with reconciled data on where capital is deployed. Partners need a clear view of funded and remaining commitments. Accurate capital call accounting substantiates liquidity and capital activity, making disciplined procedures essential for professional sponsors.

A CFO-level reporting process provides a complete view of the fund beyond its bank balance. It connects total commitments, cumulative drawdowns, current liquidity, and forecast requirements.

This level of detail builds trust. When you show exactly how much cash is left for new acquisitions, partners feel more sure. It shows that you have a grip on the fund’s life cycle.

Without this visibility, the sponsor may miss an acquisition deadline or issue a drawdown too late. Disciplined tracking supports execution and keeps investors informed. It also makes sure you follow the documented provisions in the governing documents.

Consistent investor statements and reporting cadence

Trust grows when people know when to hear from you. A steady report schedule is key. Partners expect to see how their capital is performing on a set date. These statements should be concise, consistent, and supported by reconciled data.

Statements should clearly present the fund’s assets, liabilities, equity activity, liquidity, and performance. DMR Consulting Group’s CFO services help operators establish reporting standards, management-review controls, and a dependable delivery cadence.

Quick and clear reports show that your office is strong. It demonstrates disciplined stewardship of investor capital. This is not just about math on a page.

It is about showing that you are a disciplined operator. When partners get clear reports every month or quarter, they are more likely to fund your next major investment. Consistent reporting also supports future fundraising and portfolio growth.

Using financial intelligence for sponsor decisions

Investor reporting also serves the sponsor’s internal decision process. Timely, reconciled financial information helps management evaluate funding needs, operating performance, and portfolio risk.

Variance reports show if your costs are higher than you planned. Cash flow plans tell you if you will have enough funds for the next month. This helps you decide when to call for more capital.

Variance analysis and cash forecasting help management identify emerging risks before they become material issues. For example, an unfavorable tax, insurance, or capital-expenditure variance can be incorporated into liquidity planning before the next drawdown is approved.

The same reporting framework can identify favorable performance trends and support timely capital-allocation decisions. This is the difference between maintaining historical books and using financial data as an active management tool.

When sponsors lead with reconciled data and transparent reporting, investors can evaluate the fund from a consistent information base. Well-designed reports turn transaction records into decision support for portfolio operations and future capital planning.

A practical capital call accounting checklist

A clear checklist helps real estate syndicators manage fund capital responsibly. This tool ensures your team is ready for every monthly close and capital event. You can avoid common errors that slow down your growth. Using standardized capital call accounting procedures reduces the risk that small recordkeeping errors develop into material credibility concerns.

Review governing documents and commitment schedules

Start by checking your core governing documents. Confirm each investor’s commitment before issuing a notice. Private funds often use a formal capital call to draw this capital from partners as needed. This formal step keeps everyone on the same page about their duty to the fund.

Your records should show the total pledge and the amount called to date for every partner. Most funds track these pledges as memorandum entries in a side system. They do not show up as funded contributions until the money is due. Keeping a close watch on these numbers helps you plan for future property acquisitions.

Reconcile bank activity and ledger entries

Your team should match all bank lines to your internal books. This step finds missing payments or double entries quickly. Proper capital call accounting for syndications ensures your balance sheet always shows the true cash on hand. Use this short checklist to stay on track:

- Match every bank wire to a specific partner pledge.

- Record payments on the date listed in your formal notice.

- Debit the fund investment line and credit the bank account.

- Review entries with a second team member to find errors.

Regular checks reduce liquidity gaps that could delay an acquisition closing. Set up strong internal controls for your capital process. This split of duties prevents fraud and processing errors. Good controls show your partners that you take their capital seriously and act as a good steward.

Validate investor capital and allocation records

The final step is to check your ownership split. Each new contribution may affect an investor’s capital balance or allocation. Your books must reflect these shifts to ensure profit splits are right. Reviewing these records every month keeps your fund ready for any audit or lender request.

Ask your team if the ownership data matches the latest bank wires. Does the total cash in the bank match the sum of all partner lines? Small gaps here can cause material issues when it is time to pay out profits. A tight review process keeps your fund stable and your partners confident.

Frequently Asked Questions

Is there a difference between a capital call and a drawdown?

A capital call and a drawdown generally refer to the same fund-administration event. Both terms describe a formal notice requesting that investors fund committed capital. As BT CPA explains, managers use the process for investments, expenses, or other approved fund requirements.

What happens when an investor defaults on a capital call?

The appropriate response depends on the fund’s governing documents. Accounting teams should flag the exception promptly and preserve the related notice and communications. They should also report funding status accurately in the investor subledger. Sponsors should coordinate any response with qualified advisors.

When do capital commitments appear on a fund’s balance sheet?

Uncalled capital commitments are commonly maintained in memorandum records or investor subledgers rather than recorded as cash. Balance-sheet presentation depends on the applicable accounting framework and the fund’s documented policy. Separate tracking helps management distinguish available cash from potential future funding.

How does ASC 946 affect reporting for investment funds?

ASC 946 provides specialized reporting guidance for entities that qualify as investment companies. Its provisions include fair-value measurement requirements. As Qapita explains, qualification depends on specific characteristics. Fund managers should confirm the applicable reporting framework with their accounting advisors.

Ready to talk with a real estate CFO advisor?

Poor capital call controls can create reconciliation breaks, misstated investor balances, liquidity surprises, and a loss of investor confidence. Establishing the process before the next acquisition, reporting cycle, or fund launch provides management time to define policies, assign responsibilities, and validate opening records. DMR Consulting Group helps real estate syndicators build accurate, timely reporting that supports capital planning and long-term portfolio growth.

Ready to talk with a real estate CFO advisor? Schedule a consultation to talk with a real estate CFO advisor.