Real Estate Syndication K-1 Reporting Guide

Real estate syndication K-1 reporting can become one of an operator’s most visible tests of financial discipline. Investors may not see the monthly close, account reconciliations, or allocation work behind the scenes. They do see whether their Schedule K-1 arrives with clear communication and reliable information.

Explore DMR’s real estate syndication accounting services to build a cleaner, more reliable reporting process.

Accurate real estate syndication K-1 reporting starts long before tax season. Operators need clean books, current partner records, documented allocations, coordinated tax work, and a review process that catches issues before forms reach investors. A year-round process reduces rework and gives investors clearer expectations.

If reporting is treated as a year-end project, missing data and last-minute questions can create delays. A year-round process gives the operator and tax team more time to resolve issues and helps investors plan their own filings.

What does real estate syndication K-1 reporting require?

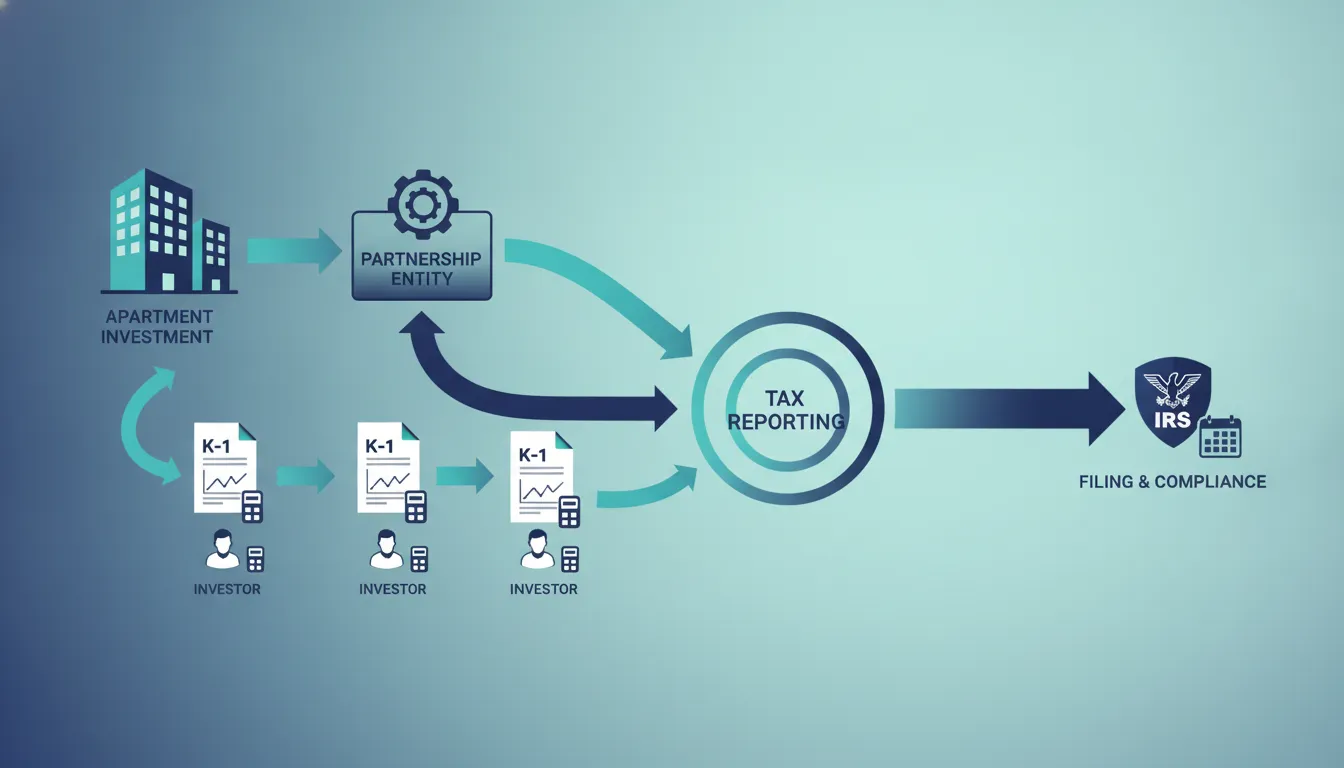

In short: A real estate syndication’s K-1 process connects the partnership return, each investor’s share of tax items, and the underlying accounting records. Operators coordinate the source data, allocation support, partner records, review, secure delivery, and investor communication.

A real estate syndication commonly operates through a partnership. The partnership files Form 1065, and Schedule K-1 reports each partner’s share of relevant tax items. The form may include income, loss, deductions, credits, and other details the investor uses when preparing a return.

The operator’s role

The tax preparer creates the partnership return and K-1s, but the operator controls much of the source information. Operators oversee the books, maintain investor records, document ownership changes, and provide the agreements that guide allocations. They also coordinate with property managers, lenders, legal counsel, and the tax team.

That makes K-1 delivery an operating process, not merely a tax-preparation task. The process should have an owner, a calendar, clear handoffs, and defined review steps.

Why good bookkeeping matters

A tax return is only as reliable as the records behind it. Unreconciled bank accounts, unclear capital activity, missing invoices, and miscoded distributions force the tax team to stop and investigate. Each open item can add time and create avoidable uncertainty.

Operators also benefit from a short variance review each month. Compare actual results with the budget and prior period, then document large or unusual changes. This routine can uncover coding errors and missing activity while records are still fresh.

Operators that need support connecting the monthly close to investor reporting can review DMR Consulting Group’s real estate syndication accounting services. The goal is a reporting system that stays useful throughout the year, not only at filing time.

Build a reliable K-1 reporting timeline

A reliable timeline works backward from investor delivery. Set deadlines for closing the books, collecting documents, validating partner data, preparing the return, reviewing allocations, correcting drafts, and delivering forms securely.

A practical timeline works backward from the expected investor delivery date. It allows time for the book close, document collection, tax preparation, operator review, corrections, and secure delivery. The dates should be agreed on before year-end and shared with each person responsible for an input.

A seven-step operator workflow

- Confirm the tax calendar. Meet with the tax team before year-end to set target dates, review filing needs, and discuss known transactions.

- Close the books. Reconcile cash, debt, fixed assets, payables, receivables, and intercompany activity. Resolve open items rather than carrying them into tax preparation.

- Collect final documents. Gather year-end statements, lender reports, property manager packages, legal documents, and records for major purchases or sales.

- Validate the partner roster. Confirm legal names, addresses, entity details, ownership periods, and transfers through a secure process.

- Review capital and allocations. Compare contributions, distributions, ownership changes, and allocation terms with the operating agreement.

- Review the draft return. Have the operator and tax team review significant variances, partner allocations, and state reporting before release.

- Deliver and communicate. Send K-1s through a secure portal, explain next steps, and give investors a clear contact path for questions.

Plan for extensions without creating confusion

An extension can provide more time to file the partnership return, but it does not remove the need for a clear plan. If an extension is likely, tell investors early. Explain what remains open, when the next update will arrive, and whether the timing may affect their personal filing decisions.

Operators should work with qualified tax advisers on deadlines and filing requirements. Dates and obligations can vary based on the entity, transaction history, and jurisdictions involved.

Which partner data should operators collect?

Operators should maintain one controlled partner master file. It should cover legal names, addresses, entity details, ownership periods, transfers, contributions, redemptions, and approved changes, with sensitive tax information collected through secure methods.

Partner data errors can affect delivery and the information shown on a K-1. A controlled intake process reduces rework and keeps sensitive information out of unsecured email threads. Operators should define how data is collected, who may update it, and who approves changes.

Maintain a current partner master file

The partner file should include each investor’s legal name, mailing address, entity type, and other information requested by the tax team. Tax identification information should be gathered and stored through secure methods. The file should also track admission dates, ownership changes, transfers, and exits.

Do not wait until forms are ready to ask whether an investor changed an address or entity. Send a confirmation request before year-end and set a firm response date. Record the source and approval for each update.

Track ownership events as they occur

Transfers, additional contributions, partial redemptions, and estate-related changes can affect allocations. Create a change log that captures the effective date, supporting document, approval, and impact on the ownership schedule. Share that log with the accounting and tax teams during the year.

A clean partner file also supports better investor service. When the portal, accounting records, and tax workpapers use consistent data, the team spends less time resolving conflicting records.

How do allocations affect each investor’s K-1?

Allocations and distributions answer different questions. An allocation assigns partnership tax items based on the agreement and applicable rules, while a distribution records cash or property paid to an investor. The two amounts may differ.

A distribution is cash paid to an investor. An allocation assigns a share of partnership tax items. Those amounts are related, but they are not always the same. This distinction is a common source of investor questions and should be explained in plain language.

Use the operating agreement as the starting point

The operating agreement describes the economic arrangement among partners. The tax and legal teams use it, along with applicable rules and the facts of the year, when determining how items should be allocated. Operators should provide the signed agreement and every amendment before preparation begins.

| Record | What it helps explain | Operator control |

|---|---|---|

| Operating agreement | Rights, economics, and allocation terms | Keep signed versions and amendments together |

| Capital ledger | Contributions, distributions, and partner activity | Reconcile it to the general ledger each month |

| Ownership schedule | Who held an interest and when | Document effective dates for every change |

| Fixed asset records | Asset additions, disposals, and depreciation inputs | Retain invoices and closing documents |

Review unusual results before release

If an investor’s allocation differs sharply from expectations, investigate before issuing the K-1. The reason may be valid, such as a transaction, a change in ownership, or the partnership’s agreed economics. The review should connect the result to source documents and tax workpapers.

Operators should not promise a specific tax result. Instead, maintain complete records and work with advisers who can apply the agreement and relevant tax rules to the partnership’s facts.

Why are syndication K-1s late or corrected?

Most late or corrected K-1s trace back to unresolved source information. Common triggers include unclosed books, incomplete property reports, missing transaction support, inaccurate partner data, ownership mismatches, and allocation questions.

Late or corrected K-1s often reflect an upstream process issue. Common causes include books that were not closed on time, missing property-level reports, unresolved transactions, incomplete partner data, and allocation questions. A correction may also be needed when new information arrives after forms have been issued.

Common causes of delays

- Bank, debt, or escrow accounts have not been reconciled.

- A property manager’s year-end package is incomplete or conflicts with the general ledger.

- Purchase, sale, refinance, or construction records are missing.

- The ownership schedule does not match capital activity.

- State filing requirements have not been confirmed.

- The tax team receives key documents too late for review.

Reduce the risk of corrected forms

Use a release checklist that covers both entity-level and partner-level information. Review major transactions, compare the current year with prior periods, and investigate unexpected changes. Confirm that partner records match the final ownership schedule and that all approved changes reached the tax team.

If a correction is necessary, communicate directly and promptly. Tell investors what changed, when the corrected form will be available, and that they should consult their own tax adviser about the effect on their return.

Year-round controls that make K-1 season easier

The strongest K-1 control is a disciplined monthly close. Reconcile accounts and capital activity, review variances, update ownership records, organize permanent documents, and surface unusual transactions throughout the year.

The most effective K-1 process is built through routine accounting work. Monthly controls create an audit trail, keep decisions visible, and reduce the number of questions left for year-end. They also give operators a clearer view of property and portfolio performance.

Close and reconcile every month

Set a monthly close schedule with owners for each task. Reconcile bank and loan accounts, review property manager reports, record capital activity, and follow up on missing documents. Use a close checklist so incomplete work is visible instead of silently rolling forward.

Keep a permanent document file

Maintain a structured repository for operating agreements, amendments, purchase and sale documents, debt agreements, fixed asset support, investor changes, and tax filings. Use clear file names and access controls. The tax team should not have to search across inboxes for key records.

Hold a pre-year-end tax meeting

Before year-end, review major transactions, ownership changes, planned distributions, open accounting items, and expected state filings with the tax team. This meeting creates time to gather support while the people involved still have the details close at hand.

DMR Consulting Group provides accounting and CPA services designed around real estate investors. Operators can also review DMR’s broader real estate investor financial services to coordinate accounting, tax, and advisory needs. A coordinated process can help turn year-end reporting from a scramble into a managed workflow.

How should operators communicate with investors?

Useful investor communication is specific, scheduled, and secure. State the target delivery date, explain open dependencies, commit to the next update, and separate portal-support questions from tax questions.

Investor communication should be consistent, specific, and timely. Avoid vague promises such as saying K-1s will arrive “soon.” Give a target date, explain whether any dependencies remain, and state when investors will receive the next update.

Set expectations before tax season

Include the reporting process in onboarding materials and annual communications. Explain how K-1s will be delivered, which investor details must be confirmed, and where questions should be sent. Remind investors that they should discuss their own filing choices with their tax advisers.

Use secure delivery and a clear support path

Send tax forms through a secure portal rather than ordinary email. Give investors simple instructions for access and identify the right contact for portal issues versus tax questions. Track delivery and returned messages so problems are resolved quickly.

If the timeline changes, send an update before the prior target date passes. A short, factual update protects trust better than silence, even when the final answer is not yet available.

Frequently asked questions about syndication K-1 reporting

What is a K-1 in a real estate syndication?

Schedule K-1 reports a partner’s share of certain partnership tax items. Investors use the form when preparing their own returns. It is different from a cash distribution statement because taxable allocations and cash paid may not match.

When should operators start preparing for K-1 reporting?

Preparation should happen throughout the year. Monthly reconciliations, current partner records, organized transaction support, and a pre-year-end meeting reduce the volume of unresolved work during tax season.

Why might an investor receive a corrected K-1?

A corrected K-1 may be needed when new or revised information changes the partnership return or an investor’s reported items. Operators should explain what changed and advise investors to consult their own tax professionals.

Can operators guarantee when every K-1 will be delivered?

Operators can set and manage a target timeline, but outside information and unresolved tax issues may affect it. The best approach is to build a disciplined process and communicate changes early.

How can an operator improve the K-1 process?

Start with clean monthly books, a reconciled capital ledger, controlled partner-data updates, organized documents, and clear tax-team deadlines. Review drafts before release and use a secure investor portal.

Make K-1 reporting a year-round operating strength

Reliable real estate syndication K-1 reporting gives operators more than a tax-season deliverable. It creates better records, clearer investor communication, and stronger financial control across the partnership.

DMR Consulting Group combines real estate investor experience with data-driven accounting and tax services for real estate investors. Schedule a consultation to discuss a reporting process built around your syndication’s needs.