Rent Roll Analysis for Real Estate Investors

Rent roll analysis turns a tenant list into an investor decision tool. Before you buy a rental property, recapitalize a portfolio, or approach a lender for refinancing, the rent roll helps you test whether reported income is stable, collectible, and likely to hold up after closing. It shows occupancy, lease expirations, delinquency, market rent gaps, and cash flow risk at the unit level instead of hiding them inside a single revenue line.

A strong rent roll review does not stop at adding monthly rent. It reconciles what tenants should pay, what they actually pay, when leases roll, and how those facts affect net operating income, debt service, and valuation. That is why investors should review the rent roll alongside trailing operating statements, lease documents, and property-level financial reporting before making acquisition or refinance decisions.

What Is Rent Roll Analysis?

Rent roll analysis is the process of reviewing a property’s tenant, unit, rent, lease, and collection data to judge the quality of rental income. A rent roll usually lists each occupied or vacant unit, tenant name, lease start and end dates, scheduled rent, deposits, concessions, and delinquency status. Investors use that data to verify revenue assumptions and find risks that a summarized profit and loss statement cannot show.

For a real estate investor, the rent roll answers five practical questions:

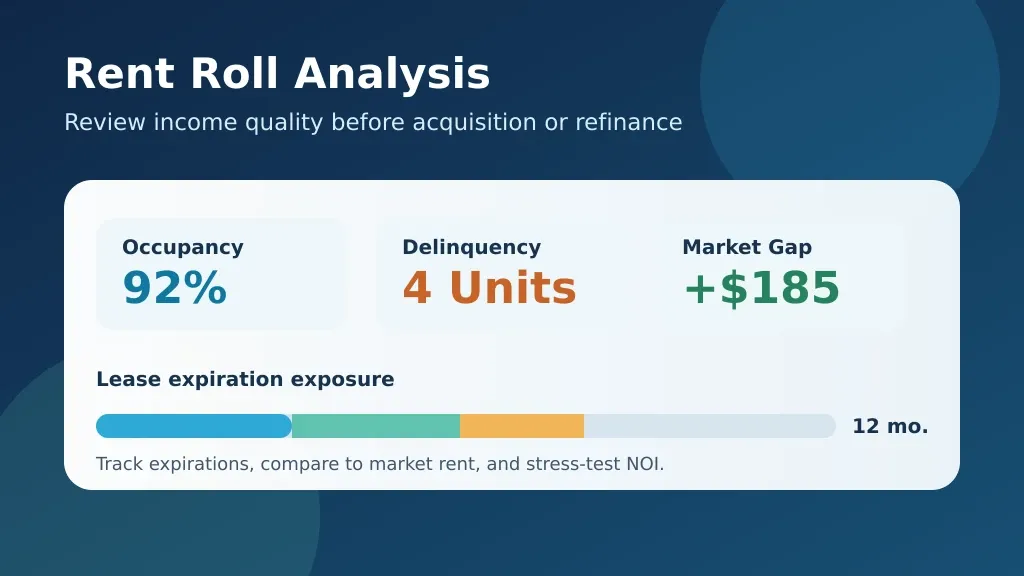

- Occupancy: How much of the property is leased, and how much income is truly being collected?

- Lease rollover: Which leases expire soon, and how much cash flow depends on those renewals?

- Delinquency: Which tenants are behind, and is bad debt being understated?

- Market rent gaps: Are units below market, at market, or carrying above-market revenue that may reset lower?

- Cash flow risk: Would the property still support expenses and debt service if collections weaken or renewals miss expectations?

The rent roll is not a standalone verdict. It becomes more powerful when checked against bank deposits, the trailing twelve-month income statement, general ledger detail, lease files, and property management records. DMR’s real estate accounting and CPA services focus on building this kind of clean financial foundation so owners can act on reliable reporting instead of estimates.

Why Rent Roll Analysis Matters Before Acquisition or Refinancing

A property can appear attractive in a broker package while its unit-level income tells a weaker story. A 95% physical occupancy figure may coexist with delinquent tenants, concessions, stale rent increases, or leases expiring right before a loan closes. Rent roll analysis brings those conflicts into view early enough to change underwriting, renegotiate price, request reserves, or pause the transaction.

For acquisitions

During acquisition due diligence, rent roll analysis validates the revenue used in valuation. Investors can identify vacant units treated as “leased,” rent increases assumed but not executed, tenants on month-to-month terms, and leases that do not match the seller’s summary. Those findings affect normalized NOI, cap-rate valuation, rehab priorities, and post-close working capital needs.

For refinancing

During a refinance, lenders care about income durability. A rent roll with large near-term expirations, recurring delinquency, or above-market leases can make cash flow look less dependable. Investors who prepare a clear lease schedule, document collections, and explain market-rent assumptions are better positioned to support the story behind debt service coverage.

For ongoing portfolio management

Owners with multiple properties should treat the rent roll as a recurring management report, not just a transaction document. It can flag units due for renewal outreach, delinquency trends by property, and rent gaps that deserve a measured pricing plan. As portfolios scale, DMR’s broader real estate investor financial systems guidance explains why disciplined reporting matters more than scattered spreadsheets.

Rent Roll Fields Investors Should Review First

The right rent roll format depends on property type, but every investor review should organize the data so a reviewer can move from unit-level facts to property-level conclusions. At minimum, examine these fields:

| Field | What to Verify | Why It Matters |

|---|---|---|

| Unit or suite | Every rentable unit appears once and vacant units are not omitted | Prevents occupancy from being overstated |

| Tenant status | Occupied, vacant, notice, eviction, employee, or model unit | Separates true revenue from non-revenue occupancy |

| Lease start and end dates | Dates agree to signed leases and renewal documents | Builds a reliable expiration schedule |

| Scheduled rent | Rent agrees to the lease and any approved increase | Tests reported gross potential rent |

| Collected rent | Payments reconcile to receivables and deposits | Measures economic occupancy and bad debt |

| Concessions or credits | Free rent, discounts, and credits are disclosed | Prevents net rent from being inflated |

| Security deposit | Deposit records are complete and support liability balances | Reduces closing and balance sheet surprises |

| Market rent estimate | Comparable units use a consistent basis | Frames upside and rent rollback risk |

If a seller or manager cannot produce these basics cleanly, treat that as a diligence signal. The issue may be administrative rather than fatal, but unreliable source data creates avoidable underwriting risk.

Step-by-Step Rent Roll Analysis Checklist

-

Reconcile the rent roll to financial statements

Start by comparing scheduled monthly rent on the rent roll with rental income reported in the general ledger and trailing operating statement. Then compare actual collections with bank deposits or property management reports. Differences deserve a written explanation, especially if the underwriting model relies on scheduled rent rather than cash collected.

-

Separate physical occupancy from economic occupancy

Physical occupancy measures leased or occupied units. Economic occupancy measures income collected relative to income that could have been collected. A building can be physically full but economically weak if collections lag, concessions are heavy, or tenants are paying partial rent. Investors should calculate both rather than accepting a single occupancy number.

-

Build a lease expiration schedule

Group lease expirations by month or quarter for the next twelve months, then by year for longer-dated leases. Flag periods where a high share of rent can roll at once. Concentrated expirations create leasing cost risk, vacancy risk, and potential refinance timing issues.

-

Review delinquency and collection quality

Identify tenants with unpaid current rent, recurring late payments, payment plans, or balances that continue to age. Compare the delinquency schedule with bad debt expense and cash receipts. If one report calls a tenant current while another shows an old receivable, ask which source is correct before trusting NOI.

-

Compare in-place rent to realistic market rent

For each unit type, compare existing rent with recent signed leases, true comparable properties, and the property’s condition. Below-market rent may suggest upside, but it is not guaranteed. Above-market rent may indicate rolldown risk at renewal. Do not use a single market-rent assumption for renovated and unrenovated units without support.

-

Stress-test cash flow risk

Translate rent roll findings into underwriting scenarios. What happens if near-term expirations renew flat instead of at the projected increase? What if delinquent units turn vacant? What if vacancy downtime stretches longer than expected? The point is not to assume failure; it is to quantify how thin or resilient the investment thesis is.

Metrics That Make a Rent Roll Decision-Ready

An investor does not need dozens of metrics to make the rent roll useful. A short dashboard tied to the underwriting model is usually better than a long list without decisions attached.

| Metric | Simple Formula | Decision Use |

|---|---|---|

| Physical occupancy | Occupied rentable units ÷ total rentable units | Measures visible vacancy pressure |

| Economic occupancy | Collected rental income ÷ gross potential rent | Captures concessions, delinquency, and bad debt |

| Delinquency rate | Past-due tenant balance ÷ monthly scheduled rent | Shows collection risk not visible in occupancy |

| Near-term lease rollover | Rent expiring in next 12 months ÷ total scheduled rent | Highlights renewal and downtime exposure |

| Market rent gap | Market rent minus in-place rent, by unit or segment | Frames upside or rent rollback risk |

| Revenue concentration | Largest tenant rent ÷ total rent | Important for commercial or mixed-use deals |

Residential investors may focus more on unit turnover, collections, and rent-gap execution. Commercial investors may need heavier tenant concentration, weighted lease term, expense recovery, and option analysis. The principle is the same: use rent roll data to isolate revenue assumptions that materially affect cash flow.

How to Review Occupancy Without Missing Income Problems

Occupancy is often the headline, but it can be misleading when treated as the whole story. Review it in three layers:

- Physical occupancy: Are units occupied or vacant?

- Leased occupancy: Are signed leases in place, even if move-in has not occurred?

- Economic occupancy: Is revenue actually collected at the assumed level?

For example, a 20-unit property with 19 occupied units may look strong at 95% physical occupancy. If two tenants are materially delinquent, one occupied unit is discounted through concessions, and a fourth has a month-to-month lease likely to leave, the income risk is higher than the headline suggests. Rent roll analysis forces underwriting to reflect that difference.

Lease Expirations: Find Rollover Risk Before It Hits NOI

Lease expirations matter because an expiration is both an opportunity and a threat. A below-market tenant renewing at higher rent can lift cash flow. A tenant leaving unexpectedly can add make-ready costs, leasing costs, vacancy downtime, and lost revenue.

Create a lease expiration schedule and answer these questions:

- How much scheduled rent expires within 3, 6, and 12 months?

- Are expirations concentrated in one season or one property segment?

- Which expiring tenants are below market, above market, delinquent, or likely to non-renew?

- Does the business plan assume rent lifts before the owner has proof those renewals are achievable?

- Would rollover weaken cash flow during a refinance, capital call, or acquisition transition period?

Investors should avoid treating every expiration as automatic upside. Rent increases only become real when demand, unit condition, tenant quality, and collection behavior support them.

Delinquency: The Fastest Way Reported Rent Diverges From Cash

Delinquency deserves its own section because it is easy to bury in receivables while still showing contractual rent on the rent roll. Review current balances, 30-, 60-, and 90-day aging, recurring late payers, legal status, and write-off policy. Then ask whether the revenue model assumes full rent from tenants whose payment history says otherwise.

When delinquency is concentrated, classify the problem before changing the model:

- Temporary timing: One-off late receipts that clear consistently within the month.

- Tenant quality: Repeated delinquency or payment plans that suggest collection weakness.

- Manager process: Inconsistent follow-up, coding errors, or unreconciled deposits.

- Market pressure: Affordability stress, higher turnover, or rents pushed beyond tenant demand.

Each root cause affects action differently. A timing issue may require reconciliation. A tenant-quality issue may require reserve assumptions. A manager-process issue may call for better accounting controls and clearer recurring reporting.

Market Rent Gaps: Upside, Rolldown, and Reality Checks

A market rent gap is the difference between current in-place rent and a supported market rent estimate. Below-market units can offer revenue growth, but only when comparables are genuinely comparable and the property can achieve the assumed rents without unexpected capital costs. Above-market units can create rolldown risk if renewal economics normalize lower.

Use these controls when assessing market rent gaps:

- Compare like-for-like unit size, condition, amenities, location, and lease structure.

- Separate achieved lease comps from advertised rents.

- Document renovation or turn costs required to reach higher rents.

- Phase rent growth realistically rather than applying an immediate portfolio-wide increase.

- Test whether higher rent assumptions reduce occupancy or slow leasing velocity.

That discipline keeps the rent roll from becoming a sales pitch. It turns a potential upside claim into an assumption the investor can defend.

How Rent Roll Findings Flow Into Cash Flow Risk

Every material rent roll issue should connect to a cash flow consequence. Investors can organize findings into a simple risk bridge:

- Starting revenue: Scheduled rent supported by executed leases.

- Collection adjustment: Delinquency, concessions, and bad debt normalizations.

- Vacancy adjustment: Current vacant units plus probable turnover from expirations.

- Rent adjustment: Supported market-rent increases or rolldown risk.

- Expense and reserve adjustment: Turn costs, leasing costs, and operational support needed to execute the plan.

- Resulting NOI and debt service coverage: The investment case after income quality is tested.

This is where property-level financial reporting becomes strategic. Investors are not just checking whether rent appears on a spreadsheet. They are deciding what cash flow is repeatable enough to underwrite, finance, and use for portfolio decisions. DMR’s finance team supports that translation from accounting records to actionable operating insight, as described in its real estate CFO services.

Common Rent Roll Red Flags

Any one red flag may be explainable. Several together should change the diligence posture.

- Rent roll total does not reconcile to the trailing income statement.

- Vacant units are missing, renamed, or treated inconsistently.

- Lease end dates are blank, stale, or do not agree with signed leases.

- Collections are weaker than scheduled rent without a clear concession or bad-debt explanation.

- Major rent growth is assumed even though recent renewals do not support it.

- A large share of revenue rolls in the next twelve months.

- Delinquency is concentrated in a handful of units that materially affect NOI.

- Security deposits, tenant credits, or concessions are tracked outside formal records.

- The property manager’s report and owner financial statements use different unit counts or revenue totals.

A Practical Rent Roll Review Example

Assume an investor is reviewing a 24-unit rental property. The broker summary states 96% occupancy and highlights potential rent increases. The rent roll review finds:

- 23 units physically occupied, but one occupied unit is on a payment plan and two have balances over 30 days past due.

- Seven leases representing a meaningful share of rent expire within six months.

- Five units are below advertised market rent, but only two have renovation scope consistent with the higher rent comp.

- The monthly rent roll total exceeds cash collections after concessions and delinquency.

The revised underwriting should not simply erase the opportunity. It should distinguish collectible current income from speculative upside, budget for turn costs, and test refinancing or debt service coverage using a realistic collection scenario. That gives the investor a better negotiating position and a clearer post-close operating plan.

Rent Roll Analysis Questions to Ask Before You Decide

- Does scheduled rent reconcile to collected rent and the general ledger?

- Are occupancy, delinquency, and concessions measured consistently across properties?

- Which lease expirations can materially alter cash flow within the next twelve months?

- Are market rent assumptions supported by achieved comparable leases, not just asking rents?

- What portion of projected NOI depends on operational improvement that has not occurred yet?

- Will the lender or investment committee see the same income quality story that management sees?

Frequently Asked Questions About Rent Roll Analysis

What is included in a rent roll?

A rent roll typically includes unit identifiers, tenants, occupancy status, lease dates, scheduled rent, deposits, concessions, and delinquency information. Sophisticated reviews also compare in-place rent with market rent and tie monthly rent to collections.

How is rent roll analysis different from reviewing a profit and loss statement?

A profit and loss statement summarizes revenue and expenses for a period. Rent roll analysis explains the tenant-level source and stability of rental income, including lease expirations, collection issues, and vacant-unit detail that summarized statements can mask.

Why does delinquency matter if the property is occupied?

Occupancy measures whether units are used. Delinquency measures whether rent is collectible. A full property with material unpaid balances can generate weaker cash flow than a property with lower physical occupancy but stronger collections.

How should investors use market rent gaps?

Use them to frame supported upside or rolldown risk, not to guarantee growth. Compare units on a like-for-like basis, document improvement costs, and model rent changes according to realistic renewal and turn timing.